The Clean Energy Economy: Is Government Investment Worth it?

A year’s worth of controversy over the bankruptcy and investigation of the high profile Solyndra Company has ushered in a debate over the government’s role in the clean energy economy.

Solyndra, a manufacturer of thin-film solar cells, was loaned $528 million from the Department of Energy’s (DOE) Loan Guarantee Program. The DOE program was created during the Bush Administration under the Energy Policy Act of 2005 and expanded by the American Recovery and Reinvestment Act in 2009. Solyndra was the largest of three solar companies given loans from the Department of Energy to go bankrupt in the past year.

Moving to prevent future failures, the U.S. House Subcommittee on Energy and Power recently approved a bill that, if ratified in Congress, would effectively end loans to innovative clean energy technology companies.

The well knows narrative of Solyndra’s failure has labeled the entire loan program a bust. Solyndra’s costly non-silicon solar panels became uncompetitive as silicone prices plummeted, while cost-saving production technology emerged. However, the entire loan program and the broader economic climate must be considered when determining the relative success of the DOE’s loan program.

Solyndra is an anecdotal piece of a much larger loan guarantee program that has successfully stimulated market growth but has not delivered prioritized job growth in the emerging clean energy market. If the government seeks to prioritize job growth in our current economic climate, policy makers must take better steps to invest in job-producing clean energy companies.

The Economic Climate for Innovative Energy Technology

What are the challenges facing an innovative energy technology company like Solyndra?

Emerging technology companies are at a significant financing disadvantage because they cannot prove the merits of their business model, which may be flawed, without large capital funds. Solyndra received these funds,but the economic climate showed the serious flaws in it’s business model.

On top of government loans, Solyndra received $949 million worth of the non-government debt and equity financing since its inception in 2005. Solyndra was backed by a number of industry leading venture capital firms, including Argonaut Private Equity, Redpoint Ventures, U.S. Venture Partners and RockPort Capital.

What the DOE and private investors could not have possibly predicted was the coming economic climate that unveiled serious flaws in Solyndra’s business model.

The 2008 financial crisis and resulting recession created cynicism toward the long-term economic outlook. Capital markets shrunk, tightening funds for capital intensive projects like solar installation, and the weakening the energy markets globally. With an economic slowdown in China and a worsening sovereign debt crisis in Europe, economic woes continue.

Start-up energy producers like Solyndra are especially disadvantaged in this economic climate because they are attempting to jump into a consumer market that is saturated with an established product; fossil fuels. By revenue, seven of the top ten largest companies in the world are oil and gas companies, selling well know and readily used products with trillions of dollars worth of built-infrastructure supporting them.

Not only are start-up U.S. energy companies attempting to compete in a market with the some of the worlds largest and most entrenched industries, they are also competing with new heavily subsidized Chinese products.

As noted in Matthew Baker’s The Biggest Challenge to American Solar Manufacturing, Chinese clean energy firms are being subsidized to the point where they were selling wind and solar modules below production costs.

Inexpensive Chinese solar and wind modules have not yet been effectively combated by U.S. tariffs as Chinese firms continue to out-compete U.S. firms. Secretary of Energy Seven Chu claims Chinese dumping along with an already weak energy market, led solar prices to drop 70 percent in two and a half years.

All of these factors surmount to huge risks for start-up energy technology firms.

Why Would the Government Attempt to Leverage Private Capital for Clean Energy?

Experts at the DOE and in the financial world assert that government policies are needed for clean energy technology companies to produce at a commercial scale. Mark Fulton, the Global Head of Climate Change Research at Deutsche Bank, claims that investors in clean energy projects need transparent long-term government programs to provide the structured framework for a better risk adjusted return on their capital investments.

As Fulton claims investment in energy technology is all about “risk and return.”

To counter the risks in investment discussed above, the DOE’s loan program backs companies with the most secure investment in the world; U.S. treasury bonds. The DOE’s loan guarantee program agrees to repay up to 80 percent of borrower’s debt obligation in the event of a default.

What is the risk to the Government?

The DOE’s loan guarantees are U.S. treasury loans and therefore are not considered government expenditures. But what about the risk of default?

According to a Bloomberg report the DOE was appropriated $2.47 billion in credit subsidy cost to cover project losses. The report stresses that the DOE’s program was designed to play for itself in applicant fees and therefore the program has not yet had budgetary implications.

To hedge against default risk, 87% of the loans of the DOE loan program’s funds went toward power generation projects that required buyers to be found in advance.

Has the DOE’s Loan Guarantee Program been Successful?

In terms of market growth the loan program has provided needed funds for many companies. There are direct ties to the loan program and the growth of the Solar industry.

The loan program, which is heavily invested in solar, has been credited with helping attract major investors to solar projects, despite the harsh economic climate. Solar investments, once thought of as a being too risky, are now more secure and profitable because of DOE loans.

Solyndra, Beacon Power and Abound Solar, the three deflating companies, represent less than 3 percent of a loan program that boasts many success stories in the solar industry.

The profitability of solar companies has also been substantially enhanced by tax credits and tariffs. Dan Reicher, executive director of Stanford University’s center for energy policy and finance claims “after tax, you’re looking at returns in the 10 percent to 15 percent range” for solar projects.

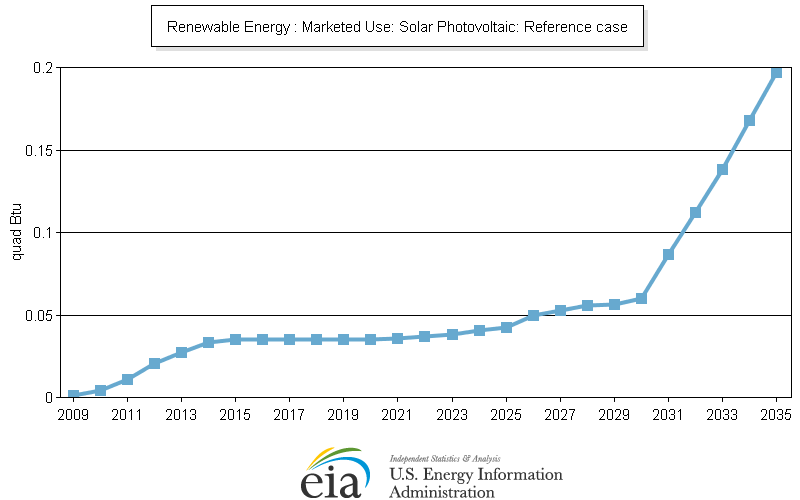

A recent report, drafted by clean-energy market analysis firm GTM Research and the Solar Energy Industries Association, showed that the value of solar systems installed in the U.S. in 2011 climbed to $8.4 billion, up from $5 billion in 2010. The report also forecasts that total U.S. installed solar power will increase 75 percent this year. The Energy Information Agency (EIA) also projects growth, as seen below.

Solar Market Use Growth –Source: EIA

Solar Market Use Growth –Source: EIA

Helping to expand the solar market, it can be asserted that the program strengthened U.S. energy security by enhancing the market share of home-grown sustainable energy. The case can also easily be made that the growth of the clean energy industry as a whole provides incalculable environmental benefits, but was this the goal of the program?

What about Jobs?

The DOE has asserted that their projects were not meant to be large job multipliers. Yet, the DOE continuously cites that their $34.7 billion in loans have helped create a total of around 60,000 permanent jobs in the industry or construction jobs.

The largest source of this job growth has been in the Advanced Technology Vehicles Manufacturing (ATMV) section of the loan program. This program has produced or saved around 39,000 jobs with $8.4 billion loaned. Still, these are not start-up clean energy technology jobs.

The $16 billion in loans designated for the 1705 section of the loan program, for innovative clean energy technology projects, is being contested in congress largely for its failure to stimulate job growth.

The funding for the 1705 program was provided by the American Recovery and Reinvestment Act in 2009. The 29 companies receiving loans from the program, not counting the three companies that went bankrupt, have produced a mere 1,174 permanent jobs. That means that a permanent job was produced for every $13.6million in DOE loans for section 1705 of the loan program.

Priorities

If job growth is the priority in clean energy technology investment, as has been frequently stated by the Obama Administration, the government should not be heavily investing in start-up clean energy technology manufactures.

From an energy security , environmental and market growth perspective the DOE’s loan program can be considered a success. Yet, the 1705 section of the loan program has not produced large job growth in clean energy manufacturing as promised.

The government should consider whether manufacturing is their aim and whether loans are the best way to leverage private capital for start-up clean energy companies, or whether direct purchases are a better option.

The leveraging of private capital is needed for future growth in the clean energy industry, especially in our current short-sighted economic climate. Our nations long-term transition away from entrenched fossil fuel is vital for our economic success and security. The government needs to do a better job of effectively communicating its priorities in this transition and determining best practices for future investment.

{kind=link}

[…] Has the DOE Loan Program Been a Failure? […]

… [Trackback]…

[…] Read More Infos here: americansecurityproject.org/blog/2012/the-clean-energy-economy-is-government-investment-worth-it/ […]…